As an alternative to buying life insurance through a provider or adviser, many Australians choose instead to hold their insurance cover through their superannuation fund. While this is a viable option and can offer policyholders some great benefits, the majority of people simply accept this default cover without actually looking into whether it’s the right option for them.

In fact, according to CommInsure’s 2012 Life Insurance Survey, 65% of Australians settle for the default level of life insurance in their super funds – most likely because of its automatic inclusion.

It’s certainly an appealing option for a lot of people because of its low cost and little effort, but it’s also problematic because it’s leaving many people significantly underinsured – and they probably don’t even realise it.

Life insurance and super can work together to protect your livelihood and loved ones, but it requires a little more than just ticking a box on your super forms. Find out below how to make sure you’ll always be adequately covered, no matter what happens.

The Life Insurance/Super Relationship

In Australia, we’re lucky enough to have mandatory superannuation as part of our employment benefits, where 9.5% of your salary is invested into a super fund for you to access when you retire. This structure also allows super funds to arrange life insurance for their members, with the premiums paid for out of your super account balance.

Super funds – including self-managed super funds (SMSFs) – will generally offer three different types of insurance for members, which you can choose to increase, decrease or cancel depending on your individual circumstances:

- Life Insurance pays out a lump sum benefit to your nominated beneficiaries after you die.

- Income Protection Insurance provides a replacement income stream if you temporarily can’t work because of an illness or injury.

- Total and Permanent Disability (TPD) Insurance pays a lump sum benefit if you become seriously disabled and are unable to ever return to work.

Life insurance (and its associated income protection and TPD insurance) is a necessity for anyone who earns and relies on an income, and having this default level of cover within your super means that most people have at least some form of financial protection in place.

However, super funds generally only offer the minimum level of cover, so relying solely on your super for a complete protection plan usually won’t be enough. Yes, it’s probably cheaper and easier to just stick to what’s provided rather than taking out a stand-alone life insurance policy, but it comes with the risk that you may not be properly provided for when the time comes for you to claim.

If you currently have life insurance through your super fund, it’s vital that you find out all the details of the cover you have and work out whether it’s actually enough for what you need to secure you and your family’s future.

Check your product disclosure statement (PDS), contact your super fund, or talk to an insurance adviser for an assessment of the amount of cover you have vs. the amount of cover you really need.

Insuring Inside Your Super: Yes or No?

There’s no right or wrong answer. As with all life insurance options, choosing a super fund with built-in insurance has its pros and cons and needs to be considered in line with your budget, circumstances and future needs.

Pros

- It can be cheaper: Life insurance inside super is usually cheaper because super funds purchase policies in bulk, allowing them to pass their group discounts on to you.

- You won’t need to take a medical exam: Standard cover will often be automatically accepted without you having to fill in any complex forms or take a medical examination.

- Premiums are deducted from your super balance: You can choose to pay the premiums out of your super contributions rather than touch your take-home salary, so you won’t even notice paying it off.

- There are tax advantages: Paying for your insurance out of your super balance can be tax-effective as it either generates a direct tax deduction or, if you choose to salary sacrifice the cost of the premiums, is paid from pre-tax income.

Cons

- The cover is limited: The types of insurance and levels of cover available inside super is much more limited than stand-alone cover, and may not be sufficient for your needs. Life cover in super is often only for $100,000-$200,000 when realistically you may need something closer to $500,000 or $1,000,000 to adequately protect your family.

- Payout is slower: There can be delays in your benefit payouts because they go to the super fund first, which then distributes them to you or your beneficiaries, making it a more lengthy process.

- It reduces your super balance: On the flip side of paying the premiums out of your super balance rather than your take-home pay, you’ll end up with less money in your super fund for retirement.

- You may not be able to nominate your beneficiary: The Trustee of the super fund makes the final decision about the distribution of benefits, so unless you have the option of making a binding beneficiary nomination, there’s no guarantee that your life insurance payout will go to the people you want it to.

- Tax may be payable on some benefits: Beneficiaries who are not financially dependent on you will have to pay tax on the benefits they receive.

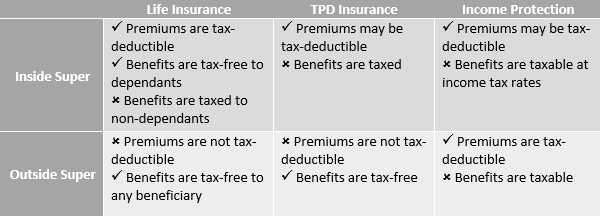

Tax Considerations

The way tax is applied to your insurance premiums and payable benefits is also different between insurance policies inside and outside your super fund. According to a Macquarie Life report on insuring through super, the tax treatment is as follows:

It’s important to carefully consider all the pros, cons and tax implications of life insurance options before deciding whether or not to have cover in your super fund. At the end of the day, it’s different for everyone and comes down to determining what’s best for you and your family’s future.

The Bottom Line

Whether you choose to have life cover in your super fund or outside of it, what it comes down to is this: do you have enough?

Any life insurance is better than none, but it’s important to know exactly how much cover you have, what your insurance provider will or won’t pay, and any other special circumstances or conditions relating to claims.

According to the CommInsure Survey, 58% of people insured through super don’t actually know the details of their cover. So if you’re currently covered through your super fund, make sure you ask. And if it’s not enough, there’s nothing stopping you from increasing your cover or taking out a second stand-alone policy outside of the fund.

When it comes down to it, it’s about your financial security and peace of mind. And that’s always worth double checking.