There are several alternatives available to you when deciding who should be the owner of your policy. While self-ownership provides the most control, in some instances it may be appropriate to place the cover inside your superannuation fund or your self-managed super fund to access tax benefits or to alleviate pressure on cashflow.

All trustees of an SMSF have a legal obligation to consider insurance for the funds members as part of the fund’s investment strategy. This includes each member’s need for Term Life, Total and Permanent Disability, and Income Protection insurance. The insurance strategy must be regularly reviewed to ensure it is appropriate for the needs of each member; this is a requirement of the Australian Taxation Office, and penalties may apply if this is not evidenced. The evidence can be as straight forward as recording the consideration process to being as complex as documenting a Statement of Advice. Failure to comply with this requirement can result in the trustee’s being fined up to $11,000.

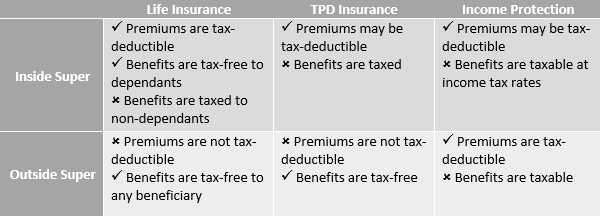

When your insurances are held within your self-managed super fund, your fund is the owner of the policy and pays the policy’s premiums. The premiums are a deductible expense to your fund and this can reduce the overall tax payable on contributions and investment income. If you make concessional contributions into your fund, then you are effectively paying the premium in pre-tax dollars.

Upon payment of the benefit, there are various issues which need to be addressed. The taxation implications upon payments will depend upon the size of the benefit, how it is paid and to whom it is paid. These issues are quite complex and planning is required.

Beneficiaries of SMSF Insurance

Where your Term Life insurance is owned by your SMSF, in order for the person you nominate as the beneficiary to receive the benefit tax free, they must be either:

- A dependant (including your current spouse – married or de facto and any natural child of any age). It can also include any other person who can prove a financial dependency.

- Your Legal Personal Representative who is essentially the executor of your estate

Death Benefit payments from an SMSF do not form part of your estate when combined with a valid Binding Death Benefit Nomination. With a valid, binding nomination, the trustee of the fund is bound to pay the proceeds to whoever is nominated (assuming they are a dependant or legal personal representative). This ensures that the policy proceeds are distributed in accordance with your wishes. Note: this is only the case where the nomination remains valid.

In the absence of a valid Binding Death Benefit Nomination, the trustee of your superannuation fund will have the discretion as to who receives the proceeds of your policy. While they will generally take any non-binding nomination into account, there is no guarantee that they will act in accordance with your wishes.

If your death benefit is paid to someone other than a dependant or your Legal Personal Representative, then there may be taxation payable on receipt of the benefit.

Limitations of Insurance Inside Your SMSF

Where your Total and Permanent Disability insurance is held within your SMSF, under superannuation legislation you may only have TPD cover with an Any Occupation definition. Today, many retail insurers offer you the option to have a “split” policy which has a linked Own Occupation component of cover held outside your SMSF and paid by you personally.

Accessing TPD benefits paid to your SMSF will incur an element of taxation on the benefits you receive. The TPD benefit paid to the fund must be paid to you personally and cannot be paid to any other members of the fund.

You can also own your Income Protection insurance within your Self-Managed Super Fund. Similarly, payments of the premiums are a deductible expense to the fund and if you make concessional contributions into you fund you are effectively paying the premium in pre tax dollars. Having said this, if you were to own the policy personally, the premiums are tax deductible to you.

Important Considerations

Whilst there is the additional advantage of alleviating pressure on your cashflow by holding your Income Protection cover in your SMSF, subject to your personal circumstances it may be more beneficial to own the policy personally due to the vast disadvantages of owning it within a super fund:

A more complex claims process – When making an income protection claim you will be required to first have the claim processed by the insurance company and then also by the super fund itself. Trustees of superfunds have an obligation to ensure that all funds released from super satisfy a condition of release. The Superannuation Industry Supervision Act (SIS Act) states that in order for a member to receive a replacement income stream from super, they will need to satisfy the temporary incapacity condition of release. This is contrasted with a policy held outside of super where a claimant simply has to meet the insurer’s requirements.

A simpler, less comprehensive product – Superannuation legislation states that income protection held inside super is only able to offer protection against a defined loss in income. In order to access the various additional benefits present in high quality Income Protection products owned outside of the superannuation environment, some retail insurers offer a “split” policy that will enable you to receive these benefits under a linked policy held personally. The benefits that you cannot be paid under a policy held in your SMSF include a trauma benefit (pays you a lump sum upon being diagnosed with one of a number of diseases) and a specific injuries benefit (pays you a lump sum should you suffer one of a number of injuries).

Indemnity contracts – Income protection held inside an SMSF can only be an indemnity style policy. What this means is that, at the time of claim, you will have to prove to the insurer that immediately prior to disability, you were earning sufficient income to justify your monthly benefit. This presents a significant hazard if you are self-employed and your income fluctuates or if, for any reason, you are earning less money than you were when you set up the policy.

Preventing payments of other insurance policies – If you have Total and Permanent Disability insurance owned inside your super fund as well as your Income Protection insurance, in the event of a total disability, you cannot claim on both your Income Protection policy and your Total and Permanent Disability policy. As previously stated, due to the SIS Act, one of the conditions of release for Income Protection is temporary incapacity; and as you cannot be temporarily incapacitated and permanently incapacitated at the same time, you cannot claim on both of the insurance policies.

It’s important to carefully consider all the pros, cons and tax implications of insurance options before deciding whether or not to have cover in your super fund. At the end of the day, it’s different for everyone and comes down to determining what’s best for you.